Fort Myers Reasonable Compensation Guide for S Corporation Owners in 2026

If you own an S corporation in Southwest Florida and work in the business, one tax rule deserves real attention: you need a reasonable salary before you take shareholder distributions . For many owners, "Fort Myers reasonable compensation" sounds like a number you can grab from a chart. It isn't.

Instead, the right wage depends on your facts. Your job duties matter. Your hours matter. Local pay matters. So does how much of the company's profit comes from your own labor.

That's why this issue matters so much for contractors, real estate-related businesses, medical practices, consultants, and service companies around Fort Myers. A salary that makes sense for one owner can be too low, or too high, for another owner with similar revenue.

What reasonable compensation means in 2026

As of March 2026, the IRS still has no new safe-harbor formula for S corporation owner pay. The agency continues to rely on long-standing rules, payroll law, and court cases. Its position remains clear in IRS guidance for S corporation officers: if a corporate officer performs more than minor services and receives payment, that payment is generally wages.

In plain English, labels don't control the result. If your company pays you for your work, the IRS may treat that money as payroll even if you called it a distribution.

Payroll mechanics still count in 2026. Wages need withholding, payroll tax deposits, and year-end forms. The 2026 employer payroll guide covers those federal rules.

A simple picture helps. Think of your S corp like a fruit stand. Wages pay you for running the stand. Distributions are what you take after the stand pays its bills, including payroll. Trouble starts when the owner works full-time, drives the revenue, and still reports a tiny salary.

That risk is real. In the Watson case, the court backed the IRS after an S corp owner took large distributions and a low salary. The lesson still fits 2026: reasonable compensation is based on facts, not owner preference.

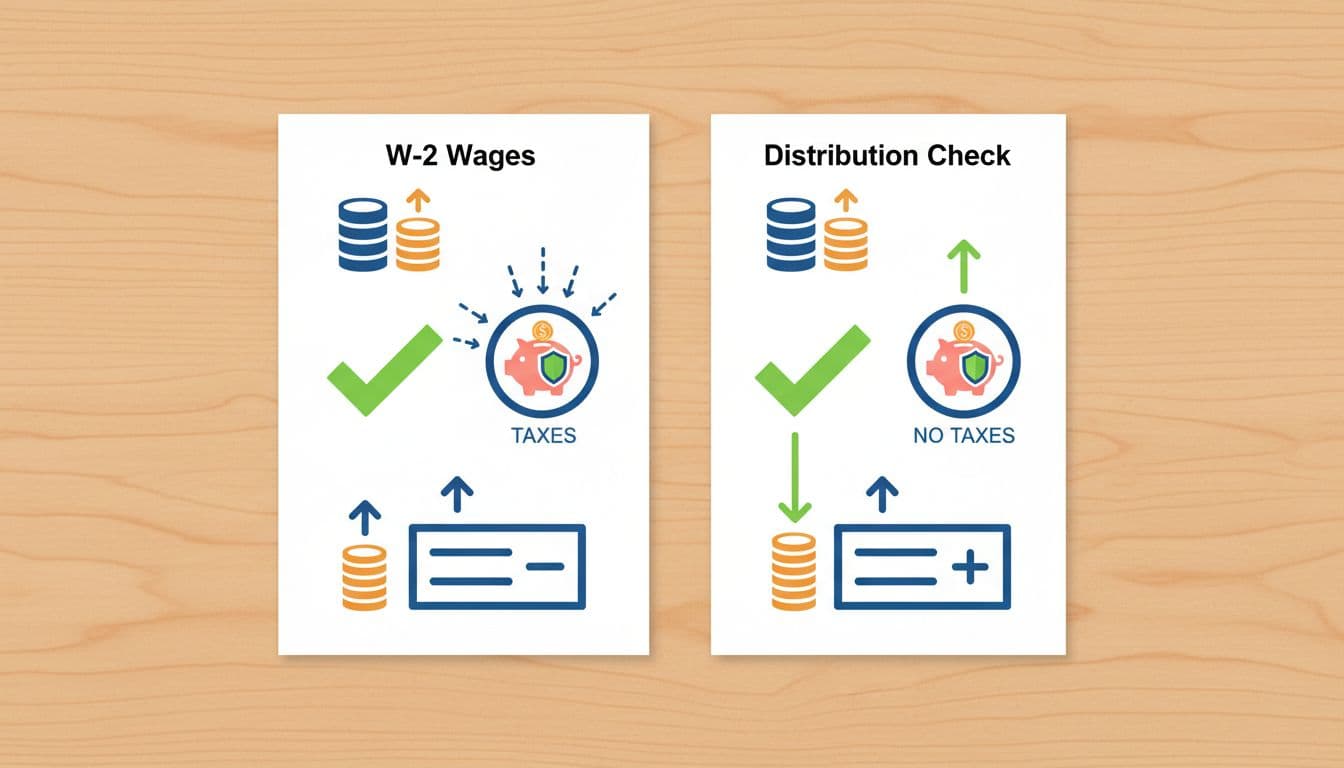

W-2 wages vs. shareholder distributions, in plain English

A W-2 wage is your paycheck as an employee of your own S corporation. It runs through payroll. Taxes come out. The business also pays employer payroll taxes. At year end, you get a W-2.

A shareholder distribution is different. It's money paid to you as an owner. It usually does not run through payroll, and it generally is not subject to Social Security and Medicare tax the way wages are. Even so, that does not make it tax-free. S corporation profits still flow through to the owner's return.

If you do the work, your S corp usually can't skip payroll and call all the money a distribution.

Here's a common Fort Myers example. A consulting owner who sells the work, performs the work, and manages client accounts will usually need meaningful W-2 wages first. On the other hand, an owner who mainly reviews reports while staff handles daily operations may support a different wage level. That's why this topic is fact-specific , not one-size-fits-all.

How to set Fort Myers reasonable compensation without guessing

Start with the work you actually do. Titles can mislead. Your daily duties tell the real story. Do you estimate jobs, supervise crews, see patients, close deals, manage marketing, answer client calls, or perform billable work yourself? The more the company depends on your personal effort, the stronger the case for a higher wage.

This quick table shows the main factors to review.

| Factor | Why it matters |

|---|---|

| Duties performed | Hands-on revenue work usually supports more wages |

| Time spent | Full-time owners need a different analysis than passive owners |

| Experience and licenses | Skilled work often commands higher market pay |

| Fort Myers market pay | Local hiring rates help support the number |

| Delegation to staff | More staff support can reduce owner labor value |

The best test is practical: what would you pay someone else to do your job in Fort Myers today? That doesn't mean a perfect clone. It means a reasonable local employee doing similar work with similar skill.

This is where business type matters. A roofing contractor who sells jobs, visits sites, and manages crews looks different from an owner who mostly reviews monthly reports. A physician-owner who sees patients daily often has a stronger wage case than an owner of a practice run by associate providers. Real estate-related firms also vary a lot. A brokerage owner who still closes deals has different facts from an owner who earns mostly from team oversight.

Avoid rigid shortcuts. The IRS has not published a 2026 percentage rule, and copying a number from social media is risky. A better file includes job notes, time estimates, payroll records, local salary data, and an explanation of why the wage fits your role.

If you're still deciding whether S corporation status makes sense at all, this article on when Form 2553 makes sense for LLCs gives helpful background.

Common mistakes that create problems

The first mistake is paying a token salary while taking regular distributions all year. The second is failing to run payroll even though the owner works full-time. Another problem is setting a salary once and never updating it as revenue, duties, or staffing change.

Timing also matters. Running little or no payroll during the year and trying to "fix it later" can create messy records. A year-end adjustment may be possible in some cases, but regular payroll is cleaner and easier to support.

Benefits can create trouble, too. More-than-2-percent shareholders have special rules for health insurance and certain fringe benefits. The IRS explains that on its IRS medical insurance rules for S corps page.

Poor documentation makes every issue worse. Without a clean paper trail, it's harder to show why your wage made sense. If the IRS reclassifies distributions as wages, you could face back payroll taxes, interest, and penalties.

Bottom line for 2026

Reasonable compensation is less about finding a magic number and more about supporting a fair one. If you work in your S corporation, pay yourself like an employee first, then take distributions after that. Disclaimer: This article is for informational purposes only and is not legal or tax advice. Your facts, payroll setup, and filing dates matter, so get advice before setting or changing owner pay.