Florida Pass-Through Entity Tax Guide for S Corps and Partnerships 2026

Florida business owners keep hearing about "PTE tax elections" and SALT cap workarounds. So it's fair to ask: does a florida pass-through entity tax exist?

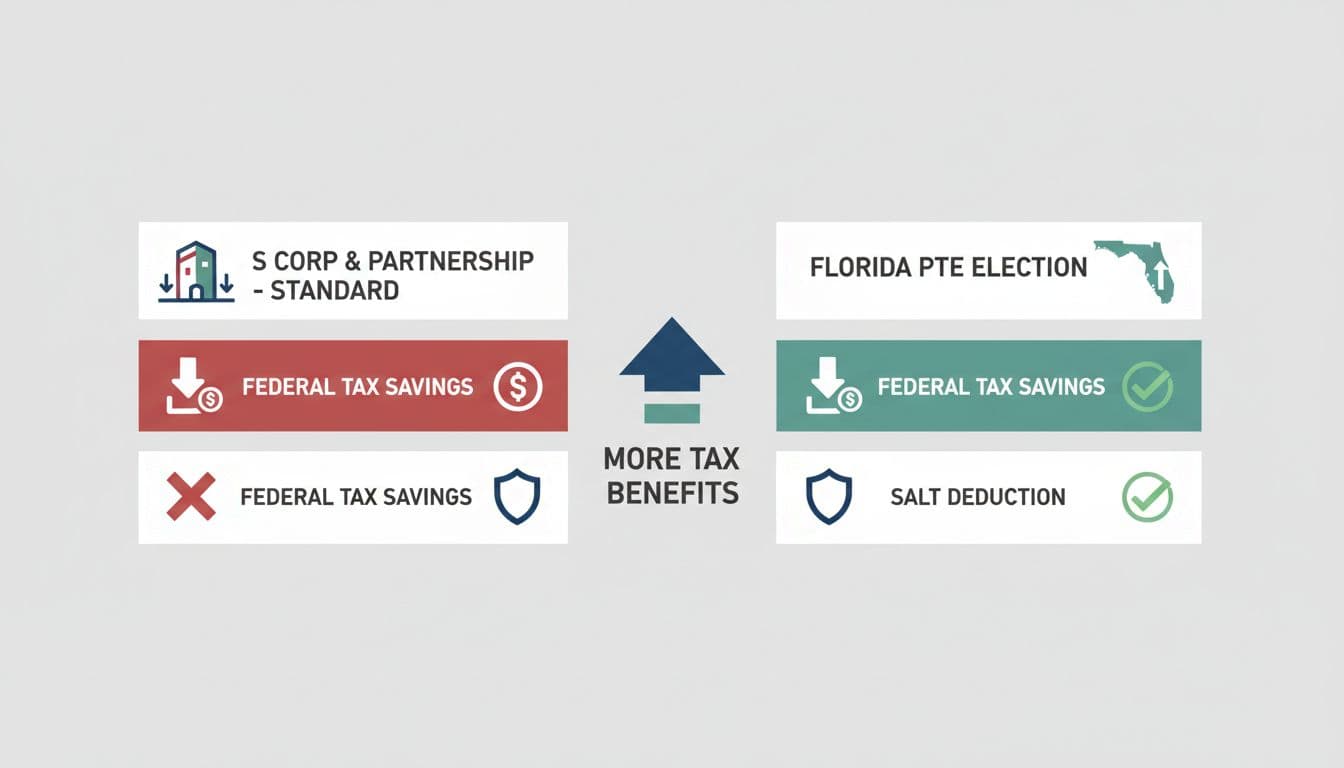

Here's the bottom line: Florida does not currently have a state-level pass-through entity tax (PTET) election like many other states. Still, the topic matters because federal rules, multi-state income, and entity choices can make "PTE tax" planning relevant for Florida S corps and partnerships.

Quick summary

- No Florida PTET election for S corps or partnerships (as of March 2026).

- PTET planning can still matter if you have owners or income in other states .

- Your real compliance focus is federal filings, K-1s, owner estimated taxes , and Florida's non-income-tax items.

Why Florida doesn't have a PTET (and why people search for it anyway)

A PTET is an entity-level state tax some states created to help owners work around the federal limit on itemized state and local tax deductions (the "SALT cap"). In many PTET states, the pass-through entity pays a state tax, then owners get a credit on their state returns. That structure may convert a limited personal SALT deduction into a business-level deduction in some cases.

Florida is different. Florida has no personal state income tax , so there's nothing for Florida to "shift" from the owner level to the entity level for most S corps and partnerships. As a result, Florida hasn't needed a PTET regime for typical pass-through income.

That said, you'll still see the phrase florida pass-through entity tax used in a few situations:

- A Florida company has non-Florida owners who pay tax in their home states.

- The business earns income in other states that do have PTET elections.

- An advisor is comparing Florida's pass-through setup to other states during expansion planning.

For Florida-only operations, think of "Florida PTET" like shopping for snow tires in Naples. It's a real product, it just isn't made for your road.

The federal SALT cap connection (and what S corps and partnerships should watch)

Most PTET conversations start at the federal level. Under current federal guidance, many states designed PTETs so that state taxes paid by the pass-through entity can be treated as a business expense at the entity level , rather than an owner's itemized SALT deduction. IRS Notice 2020-75 is commonly cited in PTET discussions as the key federal signal on this structure.

Even without a Florida PTET, Florida owners still need to keep a few federal realities in view:

First, K-1 timing drives everything . Owners can't finish clean personal returns without complete K-1s, especially when there are multiple businesses, credits, or prior-year items.

Next, estimated taxes still apply . Florida's lack of state income tax doesn't remove the federal "pay-as-you-go" rules. If owners don't have enough withholding, quarterly estimates often matter.

Finally, if your business is expanding, PTET decisions may come back into play through other states. A Florida partnership with California income, for example, may face PTET choices in California, not Florida. The best answer depends on where the income is sourced and where the owners file.

For Florida's own tax posture (mainly corporate income tax rules that apply to corporations), the Florida Department of Revenue's Corporate Income Tax overview is the most direct starting point.

2026 compliance essentials for Florida S corps and partnerships (what actually gets filed)

Because Florida doesn't impose an income tax on individuals, most S corps and partnerships operating only in Florida focus on federal compliance plus Florida's non-income-tax requirements (sales tax, reemployment tax, and entity maintenance).

Here's a simple reference table for the filings that usually drive the calendar for pass-through entities (assuming a calendar-year business).

| Entity type | Federal return | Typical Florida income tax on operating profit | Key 2026 federal due dates (TY 2025) |

|---|---|---|---|

| S corporation | Form 1120-S + Schedule K-1s | Usually none (Florida personal income tax doesn't exist) | March 16, 2026 (extend to Sept 15, 2026) |

| Partnership (incl. multi-member LLC taxed as partnership) | Form 1065 + Schedule K-1s | Usually none (same reason) | March 16, 2026 (extend to Sept 15, 2026) |

A few practical reminders help prevent "clean return, messy year" problems:

K-1s should go out on time. If owners get K-1s late, personal extensions become common, and planning gets harder.

Also, don't confuse "no Florida income tax" with "no Florida filings." Many small businesses still deal with Florida sales and use tax, reemployment tax, and local licensing depending on what they sell and how they hire.

If you want a local, entity-focused filing reference, see partnership tax filing for businesses. It's especially helpful when you're juggling 1065, K-1s, and year-end books.

When PTET planning still matters for Florida businesses (multi-state and owner-specific cases)

Even though Florida doesn't offer a PTET election, some Florida pass-through entities still run into "PTET-style" decisions. These usually show up in multi-state scenarios.

Common examples include:

- A Florida S corp sells into another state and creates income tax nexus there.

- A partnership owns real estate outside Florida and reports non-Florida income to the owners.

- Owners live outside Florida, so their home states tax their pass-through income.

At that point, the question is not "How do I elect the florida pass-through entity tax?" It becomes, "Which states tax this income, and do those states offer a PTET election that helps these owners?"

Because PTET elections can shift benefits across owners, your operating agreement (or shareholder agreement) matters. Who gets the benefit, who bears the cash cost, and how do you handle owners in different states? Those aren't "tax form" questions, they're business rule questions.

Meanwhile, Florida's corporate income tax rules can still affect you if you're not truly a pass-through for tax purposes (for example, an LLC taxed as a C corporation). For a current Florida conformity update reference, Florida DOR also posts corporate tax bulletins like Florida Corporate Income Tax Adoption of 2025 Internal Revenue Code (TIP).

End-of-year compliance checklist (S corps and partnerships)

Use this as a quick wrap-up list for a Florida pass-through entity, especially heading into filing season.

- Confirm entity tax classification (S corp vs partnership vs LLC taxed as corporation).

- Close the books monthly , not just in March, so K-1s don't become a scramble.

- Reconcile bank and credit card accounts and document owner distributions.

- Review multi-state activity (sales, payroll, property, or services performed out of state).

- Prepare and deliver K-1s on time to reduce owner extensions and amended returns.

- Check owner estimated tax needs (federal, and any non-Florida state exposure).

- Validate major deductions with good records (auto, meals, travel, contractor costs).

- Plan for extensions early (Form 7004 for the entity, then personal extensions as needed).

- Align tax and bookkeeping categories so the return matches the financials.

For a practical write-off refresher, see Fort Myers small business tax deductions. And if you're deciding between partnership vs S corp treatment for an LLC, single-member LLC tax basics helps frame the bigger picture.

Gotcha to remember: Florida not taxing your pass-through income doesn't mean other states won't. One new state filing can change the whole plan.

Conclusion

For most businesses, the florida pass-through entity tax is more myth than form, because Florida doesn't offer a PTET election as of March 2026. Still, PTET planning can matter if your income or owners cross state lines. Keep the focus on on-time federal returns, accurate K-1s, and clean books, then address multi-state issues before they turn into surprises.

Disclaimer: This article is general information, not tax advice. Facts vary by entity, owner residency, and where income is earned. Talk with a CPA or attorney before making elections or filing positions.