Fort Myers Balance Sheet Guide for Small Business Owners

Running a small business in Fort Myers means juggling beach-season rushes and off-peak slowdowns. You track sales from your shop on McGregor Boulevard or jobs across Lee County. But do you know your Fort Myers balance sheet gives a clear snapshot of your financial health right now?

Many owners focus on cash flow or monthly profits. They overlook the balance sheet. This tool shows what you own, owe, and what's left over. It helps spot cash shortages before they hit. Keep reading to learn how to read and use yours.

What a Balance Sheet Tells Fort Myers Owners

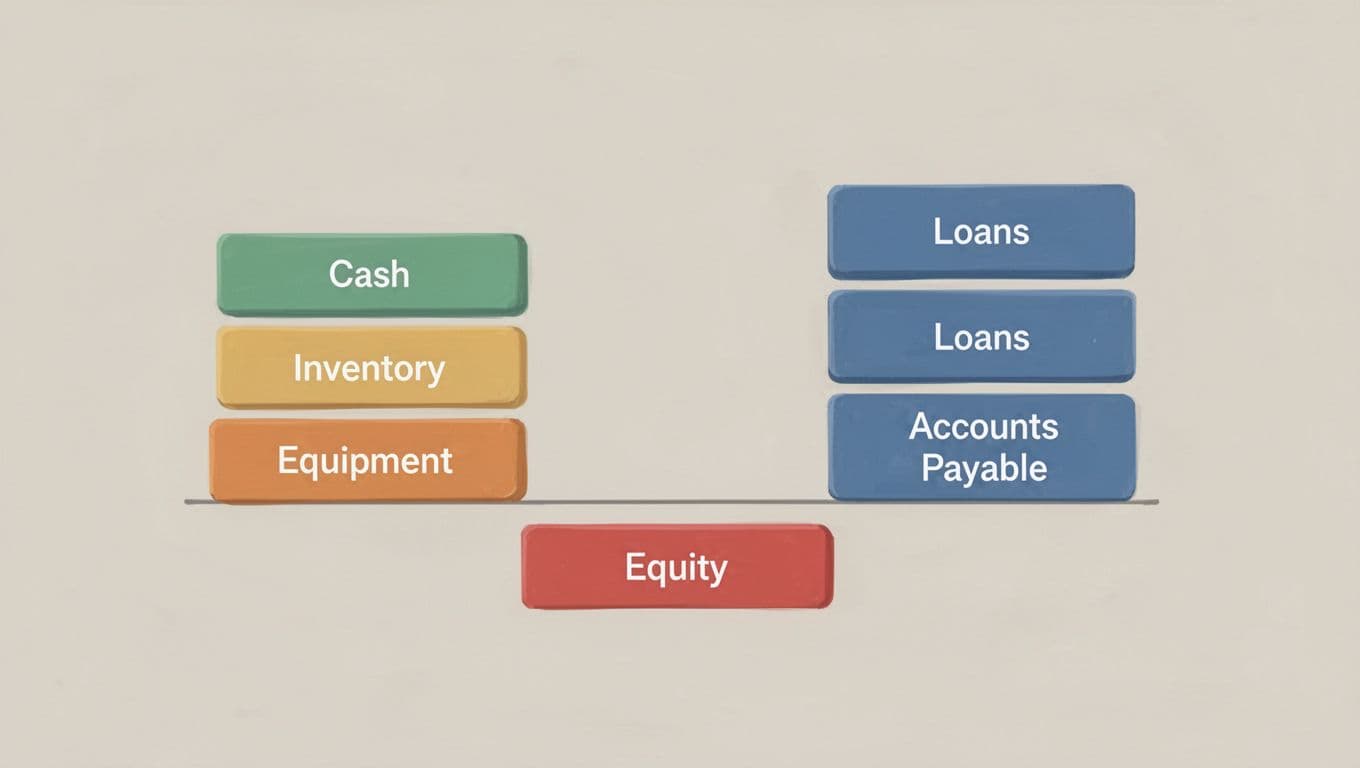

A balance sheet lists your business's position on one date. Think of it as a financial photo. Assets equal liabilities plus equity. That's the basic equation.

In Fort Myers, where hurricanes can wipe out inventory or tourism dips hurt revenue, this snapshot matters. It reveals if you have enough quick cash for repairs. Or if loans pile up too fast.

Owners use it to check stability. Banks review it for loans. It supports decisions like hiring or expanding to Cape Coral.

For help building accurate ones, check general ledger and financial statement preparation in Fort Myers.

Core Parts of Every Balance Sheet

Assets top the list. Current assets include cash, accounts receivable, and inventory. You turn these to cash fast, often within a year. Fixed assets last longer, like equipment or your Fort Myers storefront leasehold improvements.

Liabilities split the same way. Current ones, such as bills or short-term loans, come due soon. Long-term debt stretches out, like a SBA loan for growth.

Equity closes the gap. It's owner investments minus draws, plus retained profits. Positive equity means your business builds value.

Florida requires no balance sheet for most annual reports. Yet the IRS uses them for larger filers. See IRS details on financial statements for small businesses.

Short paragraphs keep this simple. You spot trends over months. Compare last quarter to now.

Sample Balance Sheet for a Fort Myers Retail Shop

Picture a local t-shirt shop near Edison Ford Winter Estates. Here's a basic example as of April 30, 2026. Numbers stay simple for clarity.

| Category | Assets ($) | Liabilities & Equity ($) |

|---|---|---|

| Current Assets | ||

| Cash | 25,000 | |

| Accounts Receivable | 10,000 | |

| Inventory | 30,000 | |

| Total Current Assets | 65,000 | |

| Fixed Assets | 50,000 | |

| Total Assets | 115,000 | 115,000 |

| Current Liabilities | ||

| Accounts Payable | 15,000 | |

| Short-term Loan | 20,000 | |

| Total Current Liabilities | 35,000 | |

| Long-term Debt | 40,000 | |

| Total Liabilities | 75,000 | |

| Owner's Equity | 40,000 | |

| Total Liabilities & Equity | 115,000 |

This shop holds $65,000 in quick assets against $35,000 due soon. Solid start. Inventory ties up cash, though.

Use small business bookkeeping services in Fort Myers to generate yours monthly.

Check Liquidity and Debt with Your Balance Sheet

Liquidity measures cash readiness. Divide current assets by current liabilities. Above, that's 65,000 over 35,000. Result: 1.86. Over 1.0 means you cover short-term needs.

Debt shows risk. Total liabilities at 75,000 equal 65% of assets. Below 50% feels safer for lenders. High debt? Cut spending or boost sales.

Overall health shines in equity growth. Rising numbers signal profits stay in the business. Track quarterly. Sudden drops flag issues like unreconciled bills.

Follow a Fort Myers bookkeeping monthly close checklist for reliable data.

Build and Maintain Your Fort Myers Balance Sheet

Start in QuickBooks or Xero. Enter transactions daily. Reconcile banks monthly. That keeps assets and liabilities true.

Outsource if busy. Local pros handle Florida sales tax liabilities too. No state income tax simplifies equity.

Lee County SBDC offers free reviews. Visit leesbdc.com or call (239) 745-3688.

This guide educates only. It's not tax or legal advice. Consult pros for your setup.

Key Takeaways for Stronger Finances

Your Fort Myers balance sheet reveals cash strength and debt loads at a glance. Review it monthly alongside profits. Adjust inventory or collections as needed.

Spot trends early. That protects against slow seasons. Build equity steadily for growth.

Strong sheets support loans from local banks. They prove your shop or service thrives. Act on the numbers today.